Loading...

ArchiveUser Experience

Reducing Confusion in APR (Annual Percentage Rate) Calculations with UX Improvements

This is an archived article from the previous version of this site. It is preserved here for reference.

Annual Percentage Rate (APR) serves as a crucial metric in the financial landscape, particularly in lending and credit. It represents the yearly cost of borrowing expressed as a percentage of the loan amount. This figure encompasses not only the interest rate but also any additional fees or costs associated with the loan, providing a more comprehensive view of what borrowers can expect to pay over time.

As a UX expert in Fintech, I recognize that understanding APR is essential for consumers to make informed financial decisions. When I delve into the intricacies of APR, I often emphasize its role in comparing different loan offers. For instance, two loans may have the same nominal interest rate, but if one has higher fees, its APR will be significantly higher.

This makes APR a vital tool for consumers seeking to evaluate their options effectively. However, many individuals find themselves overwhelmed by the technical jargon and complex calculations often associated with APR, which can lead to confusion and misinformed choices.

Key Takeaways

- APR stands for Annual Percentage Rate and represents the cost of borrowing over a year, including interest and fees.

- Traditional APR calculations can be misleading as they don't account for compounding interest and other factors.

- Confusing APR calculations can lead to consumers making uninformed financial decisions and paying more than they realize.

- Improving user experience in APR calculations involves simplifying language and presentation to make it more understandable for consumers.

- Providing clear and transparent information and utilizing interactive tools can help consumers better understand and compare APR rates.

The Problem with Traditional APR Calculations

The Lack of Transparency in Traditional APR Methods

Traditional methods of calculating APR can be convoluted and opaque, leaving consumers in the dark about the true cost of borrowing. Many lenders present APR in a way that fails to account for the nuances of individual financial situations. For example, some calculations may not include certain fees or may assume a specific repayment period that doesn't align with the borrower's actual circumstances.The Consequences of Inconsistent APR Calculations

This lack of standardization can create significant discrepancies in how APR is perceived and understood. As a result, consumers may become frustrated when trying to navigate their financial options. The complexity of APR calculations often leads to confusion, making it difficult for individuals to make informed decisions.The Need for Clearer Communication and Simplified Calculations

When faced with a multitude of figures and terms, many individuals may simply choose the option that appears most favorable at first glance, without fully understanding the long-term implications. This can result in poor financial decisions that could have been avoided with clearer communication and more straightforward calculations.The Impact of Confusing APR on Consumers

Confusing APR calculations can have far-reaching consequences for consumers. When individuals do not fully grasp what APR entails, they may inadvertently commit to loans that are not in their best interest. This lack of understanding can lead to financial strain, as borrowers may find themselves trapped in cycles of debt due to high-interest rates and hidden fees.

As a UX expert, I have witnessed firsthand how this confusion can erode trust in financial institutions and hinder individuals from achieving their financial goals. Moreover, the emotional toll of navigating confusing APR information cannot be understated. Many consumers experience anxiety when dealing with financial products, and unclear APR presentations only exacerbate this stress.

The fear of making a wrong decision can paralyze individuals, preventing them from taking necessary steps toward financial stability. By addressing these issues head-on, we can create a more supportive environment that empowers consumers to make informed choices.

Improving User Experience in APR Calculations

Enhancing user experience in APR calculations requires a multifaceted approach that prioritizes clarity and accessibility. One effective strategy involves simplifying the language used in financial documents and online platforms. By replacing jargon with plain language, I can help ensure that consumers understand what they are reading without feeling overwhelmed.

This shift not only aids comprehension but also fosters a sense of confidence among borrowers. In addition to simplifying language, I advocate for the use of visual aids to enhance understanding. Graphs, charts, and infographics can effectively convey complex information in an easily digestible format.

For instance, a visual comparison of different loan options based on their APR can help consumers quickly grasp which choice is most advantageous. By integrating these elements into digital platforms, I can create a more engaging and informative experience for users.

Simplifying the Language and Presentation of APR

The language surrounding APR often feels like a barrier for many consumers. Financial institutions frequently use terms that are not only technical but also intimidating. My goal is to break down these barriers by advocating for simpler terminology that resonates with everyday users.

For example, instead of using phrases like "finance charges," I prefer terms like "total cost" or "what you'll pay." This shift can make a significant difference in how consumers perceive and understand their financial obligations. Presentation also plays a critical role in how information is received. A cluttered layout filled with numbers and percentages can overwhelm users, leading to disengagement.

By adopting a clean and organized design that highlights key information about APR, I can guide users through the decision-making process more effectively. Utilizing bullet points or concise summaries can help distill complex information into manageable chunks, making it easier for consumers to absorb what they need to know.

Providing Clear and Transparent Information

Clear Disclosures for Informed Decisions

I strongly advocate for clear and comprehensive disclosures that outline all aspects of APR calculations, including any fees or conditions that may impact the overall cost of borrowing. This level of transparency is crucial in building trust between lenders and borrowers.Education for Empowerment

Transparency should go beyond just providing numbers; it's essential to communicate how APR is calculated and what factors influence it. By educating consumers about the components that contribute to their APR, such as credit scores or loan terms, I empower them to take control of their financial decisions.Responsible Borrowing through Knowledge

This knowledge not only enhances their understanding but also encourages responsible borrowing practices. By providing consumers with a clear understanding of APR, I aim to promote a culture of transparency and accountability in the financial industry.Utilizing Interactive Tools for Better Understanding

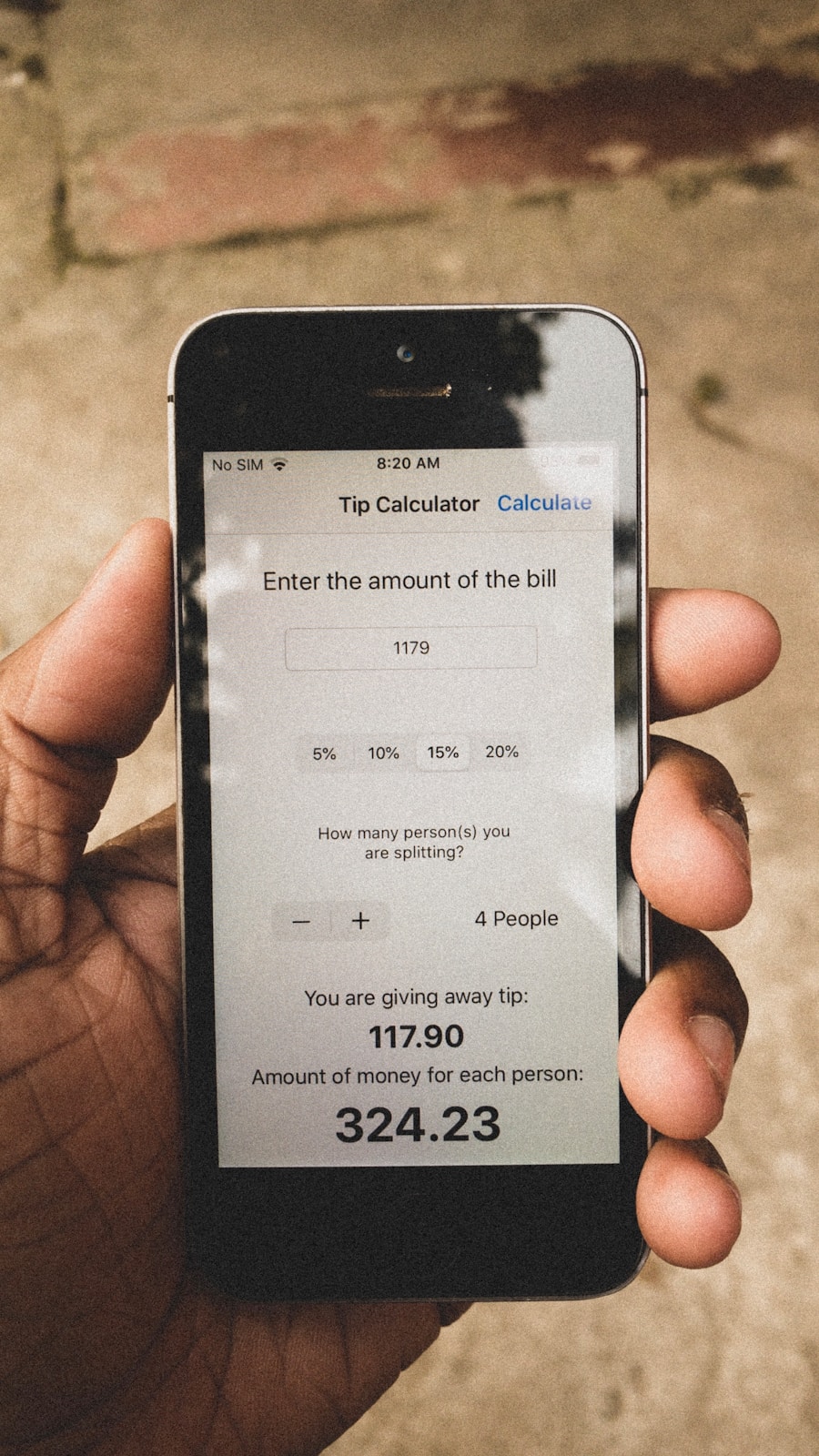

Interactive tools represent an exciting opportunity to enhance consumer understanding of APR calculations. By incorporating calculators or comparison tools into digital platforms, I can provide users with hands-on experiences that allow them to explore different scenarios based on their unique financial situations. For instance, an interactive calculator could enable users to input their loan amount, interest rate, and term length to see how these variables impact their overall APR.

These tools not only engage users but also facilitate learning through exploration. As they manipulate different inputs, they gain insights into how various factors affect their borrowing costs. This experiential learning approach fosters a deeper understanding of APR and empowers consumers to make informed decisions based on their specific needs and circumstances.

The Future of APR Calculations: Innovations and Best Practices

Looking ahead, I envision a future where innovations in technology and design continue to reshape how we approach APR calculations. The integration of artificial intelligence and machine learning could lead to personalized loan offers tailored to individual financial profiles, making it easier for consumers to find options that suit their needs without getting lost in complex calculations. Best practices will also evolve as we prioritize user-centric design principles in Fintech applications.

Continuous user testing and feedback loops will be essential in refining how we present APR information. By staying attuned to consumer needs and preferences, I can ensure that future developments remain focused on enhancing clarity and transparency. In conclusion, as I reflect on the journey toward improving APR understanding among consumers, I recognize the importance of clear communication, innovative tools, and user-centered design principles.

By addressing the challenges associated with traditional APR calculations and embracing new technologies, we can create a more informed and empowered consumer base in the Fintech landscape. The future holds immense potential for transforming how individuals engage with financial products, ultimately leading to better financial outcomes for all.

If you are interested in mastering the landscape of product strategy, a helpful article to check out is Mastering the Landscape of Product Strategy: A Guide to Navigating Obstacles and Achieving Success. This article provides valuable insights and tips for entrepreneurs looking to overcome obstacles and achieve success in their product strategy endeavors.

FAQs

What is APR (Annual Percentage Rate)?

APR stands for Annual Percentage Rate, which is the annual cost of a loan expressed as a percentage. It includes the interest rate and any additional fees or charges associated with the loan.

Why is it important to reduce confusion in APR calculations?

Reducing confusion in APR calculations is important because it helps consumers make informed decisions about borrowing money. Clear and transparent APR calculations can help borrowers understand the true cost of a loan and compare different loan options more effectively.

What are some common sources of confusion in APR calculations?

Common sources of confusion in APR calculations include complex fee structures, variable interest rates, and different methods of compounding interest. Additionally, unclear or misleading loan terms and disclosures can contribute to confusion for borrowers.

How can UX improvements help reduce confusion in APR calculations?

UX improvements, such as clear and intuitive loan disclosure forms, interactive calculators, and educational resources, can help borrowers better understand the factors that contribute to APR and make more informed financial decisions. Improving the user experience can also help borrowers navigate complex loan terms and conditions more effectively.

What are some potential benefits of reducing confusion in APR calculations?

Reducing confusion in APR calculations can lead to greater consumer trust, improved financial literacy, and more informed borrowing decisions. It can also help lenders build stronger relationships with their customers and promote a more transparent and fair lending environment.